🔄 Last Updated: 17 April 2026

The First Homes Scheme is a UK government initiative designed to help first-time buyers purchase homes at a discount of at least 30% compared to market value.

Delivered through developers and supported by Homes England, the scheme aims to improve housing affordability across England, particularly for local buyers and key workers.

That’s where the First Home Scheme comes in — a government-backed initiative designed to make buying your first home more affordable.

Government of UK official website tells about “First Homes scheme“: first-time buyer’s guidelines

MarketAppraisal tells about ” WHAT is Britain’s First Homes Scheme REALLY About?

ProTaxAccountant tells about “What Is the First Homes Scheme in the UK in 2026? “

The scheme is supported by Homes England and delivered through local authorities across England.

Table of Contents

Key Takeaways – First Homes Scheme

-

First Homes Scheme (FHS) is the evolution of affordable housing in the UK. It focuses on giving first-time buyers and key workers a real chance to get on the property ladder with discounted homes.

-

Ignoring the First Homes Scheme means missing out. Even if you qualify for other buying schemes, FHS can provide a deeper discount and greater accessibility, putting home ownership within reach faster

-

Three pillars drive FHS success: eligibility criteria (first-time buyer, income limits, local connection), discounted property prices (at least 30% below market value), and long-term affordability secured for future buyers.

-

Applying early matters. Most local authorities and developers have limited allocations, so moving quickly gives you a competitive edge in securing your dream home.

-

Think beyond Help to Buy. The First Homes Scheme works alongside other support options like Shared Ownership and Lifetime ISAs, giving you more flexibility and boosting your chances of buying your first home affordably.

In this complete guide, we’ll explain how the First Homes Scheme works, who’s eligible, how it compares to other housing support schemes, and how to apply.

First Home Scheme Buyers Guide Pdf : A First Home Scheme Pdf Guide

Who qualifies for the First Home Scheme? — eligibility checklist in 2026 → firsthomesscheme.com/first-homes-scheme-eligibility/

What Is the First Homes Scheme?

The scheme was introduced by the UK government to tackle affordability issues in the property market.

It works by offering discounted new-build homes, with the discount secured through a legal restriction registered with the HM Land Registry.

The scheme is aimed at local people and key workers, helping them stay in their communities while owning a home.

Mortgage Requirements

Buyers must secure a mortgage covering at least 50% of the discounted price.

All mortgage lending follows rules set by the Financial Conduct Authority, ensuring affordability checks are carried out properly.

The discount is permanent and stays with the property — meaning when you sell it in the future, it must be sold at the same percentage discount to another eligible buyer.

Join Our WhatsApp Group

Get instant updates, housing tips, and UK schemes directly on WhatsApp.

💬 Join on WhatsAppThe scheme is supported by Homes England and local planning authorities and is typically applied to homes built under Section 106 agreements with developers.

First Home Scheme discount — how much will you save? → firsthomesscheme.com/first-homes-scheme-discount/

Who Is Eligible for the First Home Scheme?

If you want To qualify for the First Homes Scheme, you must meet the following eligibility criteria:

✅ You Must Be a First-Time Buyer

This means you’ve never owned a property before, whether in the UK or abroad. Joint applicants must both be first-time buyers.

✅ Income Limits Apply

- £80,000 or less household income (outside London)

- £90,000 or less if you’re buying in London

✅ Local Connection Requirement

Local councils can set their own rules requiring applicants to have a local connection (e.g., living or working in the area) or give priority to key workers, such as:

- NHS staff

- Teachers

- Police officers

- Armed forces members

- Social workers

✅ Property Price Cap

The maximum price after the discount is:

- £250,000 outside London

- £420,000 in London

These limits apply to the discounted price, not the original market value.

First Home Scheme Mortgage Lenders — who will lend? → firsthomesscheme.com/first-homes-scheme-mortgage-lenders/

⚡ Get early access to government scheme updates, eligibility tips, and new build alerts — before everyone else.

📢 Join Telegram NowHow Does the First Homes Scheme Work?

Here’s how the scheme typically works in practice:

1. Find a Property

Look for a new-build property that’s part of the First Homes Scheme. Not all developers participate, so you’ll need to check with local councils or Homes England.

2. Check Eligibility

Before you reserve the home, your eligibility is assessed by the developer and local authority. You’ll need to provide documents showing income, first-time buyer status, and local connection.

3. Reserve the Property

Once approved, you pay a reservation fee and start the home buying process.

4. Get a Mortgage

You’ll still need a mortgage for the discounted price. Most lenders require at least a 5% deposit, and your mortgage must cover at least 50% of the property’s value.

5. Legal Process

The discount is secured via a legal covenant that stays with the property, even when you sell. Your solicitor will handle this.

6. Selling a First Homes Property

If you decide to sell later, you must sell it at the same percentage discount to another eligible first-time buyer approved by the local council.

Shared Ownership vs First Homes Scheme — which is better? → firsthomesscheme.com/shared-ownership-vs-first-homes-scheme/

New Towns 2026: First Homes Opportunities in 7 New Locations

In March 2026, the UK government announced the most ambitious housebuilding programme in over half a century.

Seven new town locations have been proposed across England, each delivering at least 10,000 new homes — and in some cases up to 40,000.

Every home built in these new towns will be a new-build property, which means every eligible first-time buyer will be able to apply for the First Homes Scheme discount of at least 30% off market value.

This is potentially the largest single expansion of First Homes-eligible properties in the scheme’s history.

If you are a first-time buyer — or planning to be — in or near any of these locations, this announcement directly affects your options and your timeline.

“Our next generation of new towns marks a turning point in how we build for the future — homes, jobs, transport links and green spaces designed together.”— Housing Secretary Steve Reed, GOV.UK, 22 March 2026

The 7 Proposed New Towns and First Homes Eligibility

All seven locations are proposed as new-build communities, making them directly eligible for the First Homes Scheme discount once developments are approved and construction begins.

Here is what each location will deliver:

Source: GOV.UK — Seven new towns proposed to kickstart housebuilding push, 22 March 2026

National Housing Bank — launched 1 April 2026

To fund these new towns, the government launched the National Housing Bank on 1 April 2026, backed by up to £16 billion of financial capacity. Its target is to deliver over 500,000 new homes across England.

For First Homes buyers, this means more new-build supply is coming — and more eligible properties to choose from in the years ahead.

What Are the Benefits of the First Homes Scheme?

The First Home Scheme offers several major advantages:

💰 1. Substantial Discount

With a 30%–50% discount, homes become far more affordable, especially for young families or singles struggling with high deposits.

🧍♂️ 2. Designed for Key Workers & Locals

The scheme gives priority to essential workers, helping retain local talent in expensive housing areas.

🏠 3. Long-Term Affordability

The discount stays with the property, keeping it affordable for future generations.

💳 4. Lower Deposit & Mortgage

With a lower purchase price, you need less deposit and smaller mortgage repayments.

Get Your First Home Scheme in Bristol City with 30% off—how much discount you get ? → https://firsthomesscheme.com/first-homes-scheme-bristol/

First Homes vs Other Government Housing Schemes

Let’s compare the First Homes Scheme with other popular homeownership schemes:

| Scheme | Who It’s For | Ownership Type | Discount / Support | Resale Conditions |

|---|---|---|---|---|

| First Homes | First-time buyers, key workers | Full ownership | 30–50% discount | Must sell with same discount |

| Shared Ownership | Low to mid-income buyers | Part-rent/part-own | Buy 10–75% | Buy more shares later |

| Help to Buy (Equity Loan) | New-build buyers (now closed for most) | Full ownership | 5–20% loan from gov’t | Loan repayable with interest |

| Right to Buy | Council tenants | Full ownership | Up to 70% discount | Resale restrictions apply |

| Lifetime ISA (LISA) | First-time buyers aged 18–39 | Savings scheme | 25% gov’t bonus on savings | Use for deposit only |

| Mortgage Guarantee | All buyers | Full ownership | 5% deposit allowed | No discount or grant |

The First Homes Scheme is ideal for buyers who want full ownership without needing to repay loans or share ownership.

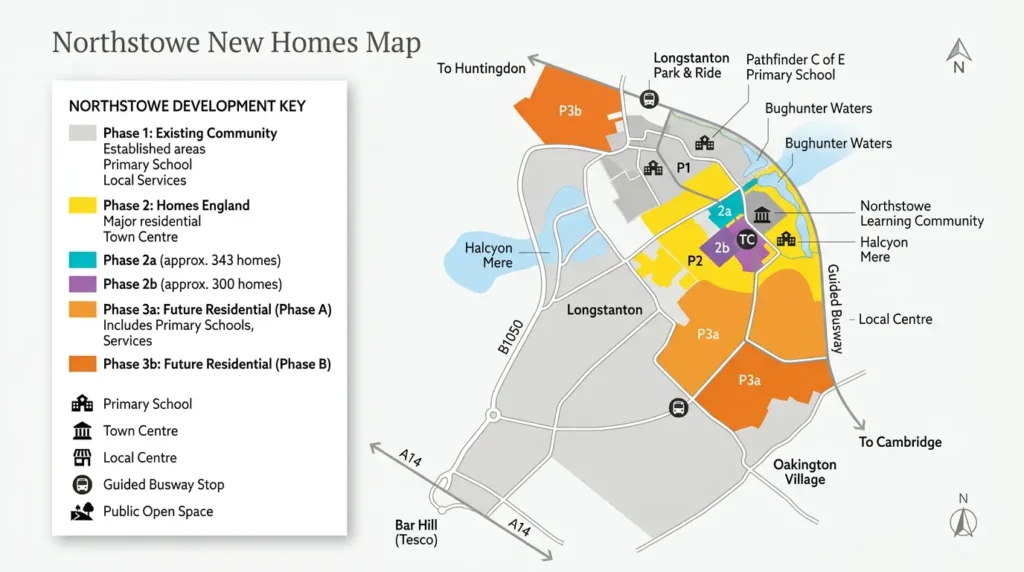

1,000 New Homes at Northstowe Region — What It Means for First-Time Buyers

According to a report published by the Cambridge Independent, a major new housing deal at Northstowe, Cambridgeshire, is great news for first-time buyers.

Homes England — the UK government’s official housing and regeneration agency — has signed a conditional contract with housebuilder Vistry to deliver 1,000 new homes, with 40% designated as affordable, directly expanding the pool of First Homes Scheme-eligible properties in the East of England.

Source: Cambridge Independent —cambridgeindependent.co.uk

Of the 1,000 homes, 900 will be built by Vistry, while two parcels of 50 homes each will be delivered by SME builders, supporting local construction businesses.

| Aspect | Key Facts |

|---|---|

| Total Homes | 1,000 (900 by Vistry, 100 by SMEs) |

| Affordable | 40% of homes |

| Timeline | Planning 2026; build starts 2027; moves from 2028 |

| Infrastructure | School, local centre, £20m+ contributions, roads/utilities/green space northstowe |

As part of the deal, more than £20 million in Section 106 contributions will fund roads, schools, utilities and green space — as confirmed by the signed planning agreement reported by the Cambridge Independent.

A planning application for the first phase is expected before the end of 2025, with building work beginning in 2027 and first residents moving in from 2028, according to the same report.

This phase (3B) forms part of Northstowe’s long-term vision of 10,000 homes across 540 hectares, overseen by Homes England.

| Benefit | Impact |

|---|---|

| Savings | Tens of thousands (e.g., DMS homes ~£310k post-discount) |

| Access | Priority for locals/key workers (first 3 months) |

| Support | SME builders + sustainable communities northstowe+1 |

For First Homes Scheme buyers, this means more new-build opportunities at a minimum 30% discount off market value, as set out under official GOV.UK First Homes Scheme guidance.

With a household income cap of £80,000 outside London and a property price cap of £250,000 after discount, Northstowe could be an accessible and affordable route onto the property ladder for local buyers and key workers across Cambridgeshire.

Real Buyer Story: How the New Towns Announcement Changes Everything for First-Time Buyers

Sarah, 32 — NHS Community Nurse, Leeds

Sarah had been saving for a deposit for four years. As a key worker, she qualified for priority access under the First Homes Scheme,

but finding an eligible new-build property near her workplace in Leeds had been difficult.

Most developments she found were either fully allocated or outside her budget.

When the government announced Leeds South Bank as one of its seven proposed new towns in March 2026, everything changed for Sarah.

The development will deliver up to 20,000 new homes — all new builds, all potentially eligible for the First Homes discount — supported by the West Yorkshire Mass Transit System.

What this means in real numbers for Sarah:

- A new-build flat valued at £200,000 in Leeds South Bank

- First Homes 30% discount brings the purchase price down to £140,000

- At a 10% deposit, Sarah needs just £14,000 instead of £20,000

- As an NHS key worker, she has priority access under local council rules

- Her mortgage repayments are based on £140,000 — not the full market value

Sarah is now registered with Leeds City Council’s housing portal and has spoken to a mortgage adviser about an Agreement in Principle.

She is waiting for the first phase of Leeds South Bank properties to be released through a participating developer.

This is an illustrative case study based on real scheme rules and the GOV.UK March 2026 announcement. Individual savings will vary depending on property price, location, and local authority rules.

How Did You Find Your First Homes Scheme Property?

Finding my First Homes Scheme UK property was a step-by-step journey as a first-time buyer looking for affordable home ownership.

🔎 Where I Started My Search

- Checked my local authority website for First Homes eligibility criteria

- Searched major UK property portals for new build homes with First Homes discount

- Contacted local estate agents about affordable housing schemes

- Spoke directly to developers offering discount market value properties

🏡 Key Steps in the Process

- Confirmed I met the income cap and first-time buyer requirements

- Got a mortgage agreement in principle from a UK mortgage lender

- Reserved a qualifying property with a 30–50% discount

- Appointed a conveyancing solicitor experienced in First Homes

What are the limitations of the First Homes Scheme???

Finding a First Homes property requires a bit of research:

🔍 Step 1: Contact Local Authorities

Your local council’s website will list new developments that include First Homes.

🏗️ Step 2: Ask Housing Developers

Major developers like Barratt Homes, Persimmon, and Taylor Wimpey often include First Homes in new developments.

🏢 Step 3: Check with Housing Associations

Some housing associations participate in the scheme or offer similar discounts.

| 🏠 Company Name | 📍 Scheme Availability | 🌐 Website |

|---|---|---|

| Barratt Homes | Nationwide (selected areas) | barratthomes.co.uk |

| Persimmon Homes | Nationwide | persimmonhomes.com |

| Taylor Wimpey | Nationwide (selected sites) | taylorwimpey.co.uk |

| Bellway Homes | Many regions in England | bellway.co.uk |

| Redrow Homes | Limited locations | redrow.co.uk |

| Crest Nicholson | South & Midlands | crestnicholson.com |

| Lovell Homes | Midlands, North, Wales | lovell.co.uk |

| Keepmoat Homes | North & Midlands | keepmoat.com |

| Bovis Homes (Vistry) | Nationwide | bovishomes.co.uk |

| Linden Homes (Vistry) | Nationwide | lindenhomes.co.uk |

Are There Regional Variations?

Yes. The First Homes Scheme only applies in England. Other UK nations have their own homeownership support:

🏴 Scotland – New Supply Shared Equity (NSSE)

- Discounted new-builds for first-time buyers.

- You buy a majority share, the government holds the rest.

🏴☠️ Wales – Help to Buy Wales / Homebuy

- Equity loans up to 20% of purchase price for new-builds.

- Local councils also offer Homebuy schemes with discounts.

🇮🇪 Northern Ireland – Co-Ownership Scheme

- Shared ownership with the ability to “staircase” to full ownership.

What the New Towns Announcement Means for You as a First Homes Buyer

If you are a first-time buyer, here is what you need to know right now:

- All new town homes will be new builds. The First Homes Scheme only applies to new-build properties. Every home built in these seven new towns will therefore be eligible once a developer registers the development with the local authority under the scheme.

- Key workers get priority. NHS staff, teachers, police officers, and armed forces members get first access in most local authority areas. If you are a key worker near any of these towns, register your interest with the local council now — before allocations open.

- London buyers have a higher price cap. For Crews Hill and Thamesmead in London, the First Homes price cap is £420,000 after discount — compared to £250,000 outside London.

- These homes are years away, but planning starts now. Final town locations are confirmed later in 2026. Construction will be phased over the coming decade. The time to save, get mortgage-ready, and understand your eligibility is today — not when the first properties are released.

- The National Housing Bank changes the supply picture. The £16 billion bank launched April 2026 is specifically designed to unlock large-scale housebuilding — meaning more First Homes properties entering the market than at any previous point in the scheme’s history.

⏰ Public Consultation — Open Until 18 May 2026

The government’s public consultation on the proposed new town locations is currently open and closes on 18 May 2026.

If you are a first-time buyer, key worker, or local resident near any of the seven proposed locations, this is your opportunity to contribute your views on housing, infrastructure, and community design.

Read the full GOV.UK announcement and consultation details →

Final new town locations will be confirmed later in 2026 following the consultation and environmental assessments.

We will update this page as decisions are announced.

Ready to Check Your First Homes Eligibility Near These New Town Locations?

Whether you are near Leeds, Manchester, London, Bristol, Bedfordshire, or Milton Keynes —

the First Homes Scheme could reduce your purchase price by 30% to 50%.

With seven new towns confirmed for consultation and over 170,000 homes in the pipeline across just these locations, the opportunity for first-time buyers has never been greater.

Use our First Homes discount calculator to see exactly how much you could save in your area, or read our full guide to eligibility criteria to find out if you qualify today.

Do Women Get Extra Benefits Under the First Homes Scheme?

While the First Homes Scheme does not offer women-only benefits, female key workers such as nurses, teachers, and social workers may get priority through local councils.

Single mothers and women in vulnerable situations can also access support and priority housing through council and housing association schemes.

| Scheme | Benefit | For Women |

|---|---|---|

| First Homes | 30–50% discount | No extra, but key worker roles (nurses, teachers) often benefit |

| Help to Buy | Govt. equity loan (closed now) | No female-specific rule |

| Shared Ownership | Buy part, pay rent on rest | Helpful for single women with low income |

| Council Housing | Affordable rent, priority lists | Priority for single mothers & abuse survivors |

| Lifetime ISA | 25% govt. bonus on savings | No direct, but useful for lower income earners |

Can the First Homes Scheme be expensive long-term?

Many buyers focus on the headline discount without considering the long-term implications. as a great way to get on the property ladder — and on the surface, it is. But many don’t realize the long-term costs.

You get a discount upfront (30–50%), but when you sell, you have to give back that percentage of the full market value — even if you’ve made improvements.

So if your home doubles in value, you owe double too.

Plus, with limited lenders, you might end up with higher interest rates and fewer options. Combine that with rising maintenance costs, potential leasehold fees, and the resale restrictions… it’s not always the bargain it seems.

The scheme offers real savings, but buyers should weigh the full financial picture before committing.

” People really need to look beyond the headline discount.

Tell me Witch region you buy Your First Homes , Comment Below!

Frequently Asked Questions (FAQs)

Can I Use a Lifetime ISA With the First Homes Scheme?

Yes! You can combine a LISA with First Homes to help with your deposit. The government adds a 25% bonus to your savings, up to £1,000 per year.

Can I Sell a First Homes Property?

Yes, but you must resell it with the same discount to another eligible buyer. The local authority will need to approve the buyer.

What If I’m Not a Key Worker?

You can still apply, but key workers and locals get priority in most areas.

Is the Scheme Available on All New-Builds?

No. Only participating developers and councils offer First Homes properties.

Can I Use the Scheme Outside England?

No, the First Homes Scheme is for England only. Check regional schemes for Scotland, Wales, or Northern Ireland.

How much discount do you get with the First Homes Scheme?

The standard discount is at least 30% off market value. Local councils can increase this to 40% or 50% if they want to make homes more affordable for local people. Here is a quick example of the savings:

£300,000 property → you pay £210,000 (30% off)

£300,000 property → you pay £180,000 (40% off)

£300,000 property → you pay £150,000 (50% off)

These are some of the largest savings available under any UK government first-time buyer scheme.

Is the First Homes Scheme the same as Help to Buy?

No — these are two separate schemes. Help to Buy (England) closed to new applications in 2023. The First Homes Scheme is still active and is currently the government’s primary affordable homeownership programme for first-time buyers in England.

Unlike Help to Buy (which involved a government equity loan), First Homes gives you full outright ownership of the property at a discounted price from day one — no equity loan to repay.

Conclusion:

Final Thoughts: Is the First Homes Scheme Right for You?

The First Homes Scheme is a game-changer for first-time buyers who meet the criteria.

If you’re eligible, it can save you tens of thousands of pounds, reduce your mortgage burden, and allow you to buy in your local area — especially valuable for key workers.

While it’s not available everywhere, and resale rules apply, the long-term affordability and full ownership make it a compelling option compared to schemes like Shared Ownership or Help to Buy.

Which region are you buying in? , Comment Below!

🔗 Ready to Take the First Step?

Check your local council’s First Homes listings, speak with housing developers, or explore your mortgage options with a trusted advisor today.

Homeownership might be closer than you think — and the First Homes Scheme could be your key to unlocking it.

Resource and Citations:

- https://www.gov.uk/guidance/first-homes

- https://www.gov.uk/first-homes-scheme

- https://henrydannell.co.uk/education-hub/blogs/first-homes-scheme-explained

- https://www.medway.gov.uk/info/200585/first_homes_scheme/1548/eligibility_criteria_for_first_homes

- https://www.dwh.co.uk/offers/first-homes/

- https://www.hull.gov.uk/regeneration-1/first-homes-scheme/2

- GOV.UK – First Homes Scheme Guidance

- HM Government – Affordable Housing Policies

- MoneyHelper – First-time Buyer Schemes

- Which? – First Homes Scheme Explained